The Venture Debt for Startups Trap: Why "Non-Dilutive" Capital Is The Most Expensive Money You’ll Ever Take

- Grow Millions

- Jan 5

- 5 min read

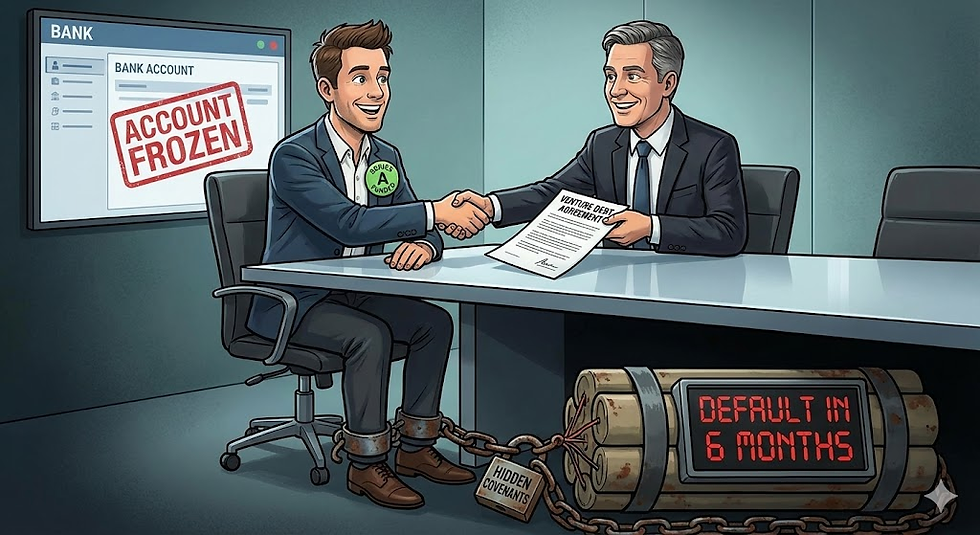

Picture the scene. You have just closed a solid Series A fundraising round. The wire transfer hits, and your bank balance looks healthier than ever. You feel flush, confident, and ready to scale.

Then, you get a call from a friendly tech banker. They congratulate you on the round and offer you an additional $3 million in venture debt for startups.

They pitch it perfectly: "It’s non-dilutive capital! It’s just an extra cushion to extend your runway and accelerate hiring. Why wouldn't you take it?"

It feels like free money. You take the deal. You use the cash to hire five new engineers and double down on marketing.

Six months later, disaster strikes. A major enterprise customer delays signing their contract by two weeks, pushing that revenue into the next quarter. Because of this single delay, you miss a minor revenue covenant milestone in your debt agreement by just 5%.

The friendly banker is suddenly not so friendly. The bank immediately declares you in default, freezes your operating accounts, and demands full repayment. Even though you still have millions in VC cash sitting in the bank, you cannot touch it. You are technically insolvent.

This is the "Venture Debt Trap." It is a scenario that plays out far too often when founders treat debt like equity, forgetting that debt comes with hard consequences.

At 3 AM, frantic founders in this position are Googling: "What happens if you breach venture debt covenants" or "Risks of venture debt for startups."

The reality is hard to swallow: Venture debt is not like a mortgage. It is jet fuel. Used correctly by sophisticated operators, it’s amazing. Used incorrectly, it explodes.

H2: What is Venture Debt for Startups, Really?

To avoid the trap, you must understand the tool. Many first-time founders conflate venture debt with venture equity, but they are fundamentally different beasts with different masters.

Venture capital (equity) is a bet on upside. VCs know most of their investments will fail, so they need the winners to win huge. If you fail, they lose their money, but they don't come after your personal assets or shut down your bank account overnight.

Venture debt for startups is a loan. Banks are in the business of risk mitigation, not upside maximization. Their primary goal is to get their principal back plus interest.

Crucially, venture debt lenders sit "senior" in the capital stack. In a liquidation event, the bank gets paid first, before VCs, before founders, and before employees. To ensure they get paid, they attach strict rules to the money.

H2: The Hidden Dangers of "Easy Money"

When you have just raised fresh equity, lenders line up to give you debt. It seems easy. But the danger lies in the fine print that most optimistic founders gloss over.

Here are the three ways venture debt for startups can become a trap.

H3: The Covenant Landmines

The biggest risk in venture debt lies in financial covenants. These are promises you make to the bank about your company's performance. They often relate to maintaining a certain cash balance, achieving specific revenue targets, or keeping your burn rate below a certain level.

If you miss a covenant, even by 1%, you are in technical default. The bank doesn't care why you missed it. They don't care that the customer promised to sign next week.

According to legal experts in venture finance, tripping a financial covenant gives the lender massive leverage, allowing them to accelerate repayment or take control of company assets.

H3: The Power to Freeze You

When you default, the bank's priority shifts immediately from "supporting partner" to "debt collector."

Because lenders usually require a blanket lien on all your company assets—including your IP and your cash accounts—they have the power to freeze operations instantly.

We have seen companies with 12 months of VC cash in the bank get shut down because a lender froze their payroll account over a minor covenant breach. The bank holds the "off switch" to your company.

H3: The Myth of "Non-Dilutive"

Bankers love to sell venture debt for startups as "non-dilutive." This is mostly true, but not entirely.

Almost all venture debt deals include "warrants." Warrants give the bank the right to buy a small percentage of your company's equity at a fixed price in the future. While the dilution is much lower than an equity round, it is not zero. It is expensive money that also costs you a slice of the pie.

H2: When Venture Debt Actually Makes Sense

Does this mean you should never take venture debt? Absolutely not. It is a powerful tool when used correctly.

The difference between jet fuel and dynamite is how you handle it.

Venture debt for startups makes sense when:

You have a clear ROI: You are using the debt to fund something with a predictable return, like acquiring a smaller competitor or financing inventory for signed purchase orders.

You use it between rounds, not instead of rounds: The best use of debt is to extend runway slightly before a planned equity raise, allowing you to hit better metrics and command a higher valuation. It should follow equity, not replace it.

Your revenue is predictable: If your sales are highly volatile, covenants will kill you. Debt is best for SaaS or subscription businesses with predictable cash flows.

H2: Navigating the Capital Stack with Growmillions.in

Taking on debt adds a layer of serious complexity to your company's financial structure. You cannot afford to manage this with back-of-the-napkin math.

At Growmillions.in, we help founders stress-test their financial models before they sign debt agreements. We can help you run scenarios to see what happens to your covenant compliance if sales drop by 20% or if a fundraising round is delayed.

We also assist founders in understanding the interplay between equity investors and debt lenders, ensuring your investor relations strategy keeps all stakeholders aligned, even when things get bumpy. We help you ensure your financial forecasting is robust enough to handle the pressures of debt repayment.

Conclusion: Treat the Banker Like an Auditor, Not a Friend

The friendly tech banker who takes you out for expensive dinners when you just raised a Series A is doing their job. They are selling a product.

But remember: when things go wrong, that banker answers to a credit committee that only cares about risk.

If you decide to take venture debt for startups, treat it with extreme caution. Negotiate the covenants aggressively. Understand the "Material Adverse Change" (MAC) clauses. And never, ever forget that the bank has the power to turn off your lights if you miss a promise on a spreadsheet.

It can be the best money you ever take, or the last money you ever take.

Comments